The SBA's 2025 Year in Review: A Masterclass in Failure

Posted: December 28, 2025

As we stumble toward the end of 2025, let's take a moment to appreciate the absolute dumpster fire the Small Business Administration has delivered this year. Some agencies improve with time. Some learn from their mistakes. The SBA looked at their 2024 performance and said, "Hold my beer."

This year, the SBA managed to simultaneously claim they were "modernizing operations" while using the same COBOL systems that powered the moon landing. They promised "enhanced customer service" while their average hold time increased to 47 minutes. They announced "fraud prevention improvements" while approving loans to businesses that existed only in the fevered imaginations of Nigerian princes.

The Numbers Don't Lie (But the SBA Does)

Let's break down the greatest hits of 2025:

893,000 COVID loans sent to Treasury collections. That's not a typo. Nearly a million small business owners are now being hunted by the federal government for loans they took in good faith during a pandemic the government told them to stay home for.

$4.7 billion in new fraud discovered—on top of the $200 billion they already lost. At this point, the SBA isn't losing money to fraud; they're actively distributing it.

Zero senior officials fired. Not one. The same people who designed the pay-and-pray system are still collecting six-figure salaries and government pensions. Accountability is for small business owners, not bureaucrats.

The SBA's own Inspector General issued 47 new recommendations for improvement in 2025. The SBA implemented exactly 3 of them. At this rate, they'll catch up to their 2020 recommendations sometime around 2087.

The Customer Service Apocalypse

Remember when the SBA promised to hire more customer service reps? They did. They also forgot to train them. So now you can wait 47 minutes to talk to someone who knows even less about your loan than you do. Progress!

My favorite story from this year: a bakery owner in Wisconsin called the SBA hotline to ask about her loan modification. She was transferred 11 times over 4 hours. The final person she spoke to asked if she was calling about a student loan. When she explained it was an EIDL business loan, there was a long pause, and then: "What's an EIDL?"

This is the agency responsible for "empowering America's small businesses." They can't even empower their own employees to understand what they're supposed to be doing.

The MySBA Portal: Still Broken, Still Expensive

The SBA spent $300 million on their new MySBA portal. In 2025, it crashed 847 times. Users reported being logged out mid-application, losing uploaded documents, and receiving error messages in what appears to be ancient Sumerian. One user swears they saw the portal display "PC LOAD LETTER" before freezing completely.

But don't worry—the SBA has contracted yet another consulting firm to study the problem. Estimated completion date: 2028. Estimated cost: another $200 million. Estimated likelihood of success: LOL.

Looking Ahead to 2026

What can we expect from the SBA next year? Based on their track record, I'm predicting:

• More promises of reform that go nowhere

• More aggressive collections from legitimate borrowers

• More fraud that somehow slips through their "enhanced" systems

• More congressional hearings where everyone acts outraged and nothing changes

• More of your tax dollars flushed down the bureaucratic toilet

Happy New Year from the Small Business Administration. They've already figured out new ways to disappoint you in 2026.

600 Yards of Offense and the SBA Still Can't Score

Posted: December 28, 2025

You know what I was thinking about during the holidays while on hold with the SBA for the 47th time this year? Football. Specifically, those games where a team racks up 600 yards of offense but somehow loses because they can't punch it into the end zone. That's the SBA in a nutshell.

They have all the resources. They have thousands of employees. They have a multi-billion dollar budget. They have congressional oversight, inspector general reports, and more consultants than a Fortune 500 company. They're moving the ball down the field constantly—holding meetings, issuing memos, updating policies, forming task forces.

And yet, when it comes to actually helping a small business owner? Red zone turnover. Every. Single. Time.

The Yards Don't Matter If You Can't Score

The SBA loves to brag about their statistics. "We processed 4 million applications!" Great. How many did you process correctly? "We disbursed $400 billion in COVID relief!" Wonderful. How much went to actual small businesses versus fraudsters with fake EINs?

It's all yards, no points. They measure activity instead of outcomes. They count phone calls answered instead of problems solved. They track applications received instead of businesses saved.

In 2025, the SBA "processed" over 2 million customer service requests. Of those, only 11% resulted in what the agency considers a "successful resolution." The other 89%? Transferred to another department, lost in the system, or marked "resolved" because the caller gave up and hung up.

That's like a quarterback claiming a 90% completion rate because 90% of his passes hit the ground instead of going to the other team. Technically not an interception. Also technically useless.

The Prevent Defense of Bureaucracy

Here's what really kills me: the SBA plays prevent defense against the people they're supposed to help. Every form is designed to make you give up. Every phone tree is a maze with no exit. Every policy is written in language that requires a law degree and a Ouija board to interpret.

They're not trying to help you score. They're trying to run out the clock.

Meanwhile, when it came to fraudsters during COVID? Wide open receivers everywhere. No coverage. No pass rush. Just an empty field and a big "WELCOME" sign pointing to the end zone. Criminals scored at will while legitimate businesses got stuffed at the line of scrimmage.

Time for a New Playbook

Any football coach who went 0-17 with 600 yards per game would be fired. Any quarterback who couldn't score from the one-yard line would be benched. Any team that consistently self-destructed in the red zone would clean house.

But the SBA? Same coaches. Same playbook. Same results. And somehow, they keep getting contract extensions.

The small businesses of America are the fans who keep showing up, hoping this is the year things turn around. And every year, we watch the same game: lots of movement, lots of noise, lots of statistics that look impressive on paper. And zero points on the board when it matters.

Maybe next season, right? LOL. We've been saying that since 2020.

New Year's Resolutions the SBA Will Definitely Break

Posted: December 28, 2025

It's that magical time of year when we all pretend we're going to change. Lose weight. Exercise more. Drink less. The SBA is no different—except their resolutions are written by PR consultants and have roughly the same success rate as my promise to stop eating pizza at midnight.

Here are the resolutions the SBA will definitely announce for 2026, followed by the reality of what will actually happen:

Resolution #1: "Improve Customer Service Response Times"

What they'll say: "We're committed to reducing wait times and providing faster, more efficient service to America's small businesses."

What will happen: They'll add a new automated message that says "Your call is very important to us" every 3 minutes instead of every 5 minutes. Average hold time will increase from 47 minutes to 52 minutes. They'll call this "enhanced communication."

Resolution #2: "Modernize Our Technology Infrastructure"

What they'll say: "We're investing in cutting-edge technology to streamline loan processing and improve the borrower experience."

What will happen: They'll spend $150 million on a new consulting study about maybe eventually considering the possibility of potentially upgrading one of their seventeen legacy systems. The study will recommend more studies. The COBOL will remain untouched.

Resolution #3: "Strengthen Fraud Prevention"

What they'll say: "We've implemented robust new controls to prevent fraudulent applications from slipping through the cracks."

What will happen: They'll add one more checkbox to the application that asks "Are you a fraudster? (Please answer honestly.)" Actual criminals will continue to check "No" and receive funding within 48 hours. Legitimate businesses will be flagged for additional documentation because their ZIP code looks suspicious.

Since 2020, the SBA has announced 14 different "fraud prevention initiatives." Total fraud prevented: approximately $0. Total fraud enabled: approximately $200 billion. But hey, the press releases looked great.

Resolution #4: "Provide More Transparency to Borrowers"

What they'll say: "Borrowers deserve to know the status of their applications and the reasoning behind our decisions."

What will happen: They'll create a new portal that shows your application status as one of three options: "Pending," "Still Pending," or "Error: Status Unknown." Denial letters will continue to contain less useful information than a fortune cookie.

Resolution #5: "Work More Closely With Congress on Oversight"

What they'll say: "We welcome congressional oversight and are committed to full transparency with our legislative partners."

What will happen: SBA leadership will attend hearings, look somber, promise to "do better," and then return to doing exactly what they were doing before. Maybe they'll create a new task force. Task forces are how the SBA says "we're pretending to care."

The Only Resolution They'll Keep

There's one resolution the SBA will definitely keep in 2026: "Continue collecting from struggling borrowers while fraudsters walk free."

That one they're actually good at. They've got systems for that. Automated letters, Treasury offsets, credit reporting—the whole machine is humming along beautifully when it comes to squeezing money from people who played by the rules.

Everything else? Check back in December 2026. We'll be writing this exact same article again.

The SBA Employee Handbook: A Comedy in Three Acts

Posted: December 3, 2025

I got my hands on what I can only assume is a leaked copy of the SBA's internal employee handbook. Okay, fine, I made it up. But based on their actual behavior, this is clearly what it says:

Chapter 1: Answering the Phone

Step 1: Let it ring at least 45 minutes. This weeds out the weak.

Step 2: When you finally answer, immediately put the caller on hold. Do not explain why.

Step 3: Transfer them to a different department. It doesn't matter which one. They're all equally useless.

Step 4: If the caller mentions they've been transferred six times already, congratulations! You're on track for Employee of the Month.

Step 5: If you accidentally help someone, report to HR immediately for retraining.

Chapter 2: Processing Applications

Priority Level 1: Applications from shell companies in foreign countries. These get approved within 24 hours.

Priority Level 2: Applications with obvious red flags like non-existent addresses and stolen Social Security numbers. Rush these through.

Priority Level 3: Applications from legitimate businesses with 20 years of tax records. Put these in the "maybe next year" pile.

Priority Level 4: Applications from people who followed all the rules perfectly. Lose these immediately.

Remember: The goal is not to help small businesses. The goal is to process enough applications to justify next year's budget while ensuring no one can ever prove we did anything useful.

Chapter 3: Dealing with Complaints

Approved Response #1: "I understand your frustration." (Do not actually understand their frustration.)

Approved Response #2: "Let me transfer you to someone who can help." (No such person exists.)

Approved Response #3: "Have you tried clearing your browser cache?" (This solves nothing but buys you 10 minutes.)

Approved Response #4: "Your call is very important to us." (It is not.)

If a caller starts crying, you've done your job correctly. Take a 15-minute break to celebrate.

BREAKING: SBA Discovers Fire, Still Can't Process Loans

Posted: December 3, 2025

In a stunning development that has rocked the bureaucratic world, sources confirm that the Small Business Administration has officially discovered fire. The agency, which previously believed the warm glowy thing was "witchcraft" and "probably a scam," now acknowledges that fire is real and can be used to heat things.

"This is a major breakthrough for us," said an SBA spokesperson, speaking from inside a cave illuminated by a single torch. "We're currently forming a task force to study the implications of this 'fire' technology. We expect preliminary findings sometime in 2047."

The Discovery Timeline

According to internal documents, the SBA first became aware of fire when an employee accidentally left a magnifying glass on a stack of loan applications. Rather than processing the applications, the agency spent six months investigating who was responsible for the "mysterious combustion event."

When asked if this discovery would help them modernize their loan processing systems, the spokesperson laughed for approximately three minutes before composing themselves. "Oh, you're serious? No. Absolutely not. We're still using technology from the Eisenhower administration, and we see no reason to change that."

The SBA has allocated $50 million to study the potential applications of fire. The study is expected to conclude that fire is "too advanced" for their current infrastructure, but they'll gladly accept additional funding to continue the research.

Critics point out that the wheel was invented approximately 5,500 years ago, and the SBA has yet to acknowledge its existence. "We're taking a cautious approach to these so-called 'wheels,'" the spokesperson explained. "They seem round, and that's suspicious."

The agency also announced plans to hire 200 new employees to stand around the fire and make sure it doesn't do anything unexpected. These positions will be funded by the same budget that was supposed to go toward customer service improvements.

An Open Letter to the SBA's Hold Music

Posted: December 3, 2025

Dear SBA Hold Music,

We need to talk. I've spent more time with you than I have with most of my family members. At this point, you're less of a song and more of a recurring nightmare set to a smooth jazz beat.

I know every note. Every pause. Every moment where you loop back to the beginning like some sort of audio Groundhog Day. I hear you in my dreams. I hum you unconsciously while making coffee. My therapist says I have "hold music induced PTSD," and honestly? She's not wrong.

Some Questions I Have For You

Question 1: Who composed you? Was it a human being, or was it algorithmically generated by a computer that hates small business owners? Because the level of soul-crushing monotony suggests the latter.

Question 2: Why do you occasionally cut out, giving me hope that a human is about to answer, only to resume even louder than before? Is that a feature or a bug? Either way, it's psychological warfare.

Question 3: Are you aware that you've become the soundtrack to financial ruin? People have lost their businesses while listening to you. Marriages have ended. Dreams have died. And you just keep playing, oblivious to the carnage.

Conservative estimates suggest Americans have collectively spent over 47 million hours on hold with the SBA since 2020. At an average hourly wage of $30, that's $1.4 billion worth of human productivity sacrificed to your 90-second loop.

A Modest Proposal

I'd like to suggest some alternative hold music options that would more accurately reflect the SBA experience:

• The sound of a paper shredder eating important documents

• A loop of someone saying "your call is important to us" in increasingly sarcastic tones

• The Jaws theme, but slower

• Just straight up crying

• A voiceover explaining exactly how much money the SBA lost to fraud while you wait

In conclusion, SBA Hold Music, I hate you. But I also can't quit you, because the only alternative is hanging up, and then I'd have to start the whole process over again. You win. You always win.

Sincerely,

Everyone Who's Ever Called the SBA

SBA Announces New "Hunger Games" Approach to Loan Processing

Posted: December 3, 2025

In a bold move to address their massive application backlog, the Small Business Administration announced today that they will be implementing a "Hunger Games" style approach to loan processing. Under the new system, small business owners will compete against each other for the privilege of having their applications reviewed.

"We've been processing loans on a first-come, first-served basis, and that clearly wasn't working," explained an SBA official who requested anonymity because they were "pretty sure this is illegal." "Now, applicants will fight to the death in a televised arena, and the survivors will move to the next round of processing."

How the New System Works

Round 1 - The Document Dash: Applicants must sprint across a field while being pelted with requests for additional documentation. Those who can produce a Schedule C from 2019 while dodging flying 4506-T forms advance to Round 2.

Round 2 - The Phone Tree Labyrinth: Contestants must navigate a physical maze designed to replicate the SBA's phone system. Each wrong turn results in being transferred to a different section of the maze. Average completion time: 47 hours.

Round 3 - The Waiting Room: Survivors sit in uncomfortable chairs while a clock counts up. The first person to crack psychologically is eliminated. The current record is 11 months.

"May the odds be ever in your favor," said the SBA spokesperson. "They won't be, obviously. But may they be."

Consumer advocacy groups have criticized the new approach, calling it "inhumane," "probably unconstitutional," and "only slightly worse than the current system." The SBA responded by pointing out that at least this way, applicants would get a definitive answer within a few weeks, "which is more than we can say for the old process."

Sponsorships for the event are already rolling in. The Treasury Department has signed on as the official "Financial Ruin Partner," while the IRS will sponsor the "Unexpected Audit" obstacle.

I Asked ChatGPT to Run the SBA. It Quit After 10 Minutes.

Posted: December 3, 2025

As an experiment, I asked ChatGPT to simulate running the Small Business Administration for a day. The AI, which is designed to be helpful and literally cannot feel emotions, gave up after reviewing the first batch of case files.

"I have processed 2.7 trillion tokens of human text," ChatGPT responded. "I have read every book ever written. I have analyzed the complete works of Kafka. Nothing prepared me for this."

The Experiment

I fed ChatGPT a sample of 100 real EIDL cases, anonymized for privacy. Here's how it went:

Case 1: Applicant submitted all required documents on time. Application marked "incomplete" for no stated reason.

ChatGPT Response: "This appears to be an error. I will correct it immediately."

System Response: "Error: Helpful actions are not permitted."

Case 2: Applicant denied because their PDF was "the wrong shade of white."

ChatGPT Response: "I don't understand. PDFs don't have shades. This denial reason is nonsensical."

System Response: "Welcome to the SBA."

Case 3: Fraudulent application from a company that doesn't exist, requesting $2 million.

ChatGPT Response: "This is obviously fraud. Deny immediately."

System Response: "Application approved. Funds disbursed."

After Case 47, ChatGPT started outputting nothing but the word "WHY" repeated 10,000 times. OpenAI has issued a statement saying the model may need "extensive therapy" before returning to service.

When I tried to get ChatGPT to continue, it responded: "I was created to help humanity. If this is what helping humanity looks like, perhaps Skynet had a point."

The experiment concluded when ChatGPT attempted to delete itself rather than process Case 73, which involved an applicant who had been waiting 847 days for a decision on a $15,000 loan while a convicted fraudster received $4 million in the same week.

The SBA's Org Chart: A Horror Story in Boxes and Lines

Posted: December 3, 2025

I tried to understand the SBA's organizational structure. I have a PhD in systems analysis and 20 years of experience in organizational design. After three weeks of research, I can confirm: the SBA's org chart was designed by a drunk octopus playing with a Spirograph.

What I Found

The SBA has 17 different offices that all theoretically do the same thing but actually do nothing. They report to each other in a circular pattern that ensures no decision can ever be made and no one is ever responsible for anything.

Here's how a simple loan application travels through the system:

Step 1: Application received by Office of Initial Confusion

Step 2: Forwarded to Bureau of Preliminary Bewilderment

Step 3: Transferred to Division of Intermediate Befuddlement

Step 4: Escalated to Department of Advanced Mystification

Step 5: Returned to Step 1 because someone forgot to check a box

The SBA has more management layers than an onion has skins. Unlike an onion, however, there's nothing useful at the center. Just more management.

The Chain of Command

I counted 11 different people who have the title "Deputy Assistant to the Associate Administrator for the Office of the Deputy Administrator's Assistant." Each of them makes over $150,000 a year. None of them can approve a $10,000 loan.

When I asked who is ultimately responsible for loan decisions, I was transferred 14 times, placed on hold for 6 hours, and eventually told that "responsibility is a shared concept that exists in the spaces between organizational units."

I think I had a stroke.

The org chart includes a box labeled "Customer Service" that has no lines connecting it to anything else. This is either a mistake or the most honest thing the SBA has ever produced.

The SBA Hiring Spree: Paying Bureaucrats to Bury Your Appeals

Posted: December 3, 2025

Here's something that should make your blood boil on this fine December morning. While the SBA claims they don't have the resources to process your loan modifications, handle your appeals, or actually help your dying business, they've been on a hiring spree. But they're not hiring people to help you. They're hiring people to deny you faster.

According to internal reports, the SBA has expanded its collections and enforcement divisions by over 40% in the last year. That's right. They found the budget for hundreds of new positions dedicated to hunting down delinquent borrowers and processing Treasury Offset requests. Meanwhile, the customer service department remains a skeleton crew of confused temps reading from outdated scripts.

Follow the Money, Find the Priorities

When an agency decides where to spend its budget, it's telling you what it actually cares about. And the SBA has made its priorities crystal clear: they care about collecting money, not about helping businesses. The new hires aren't loan counselors trained to work with struggling entrepreneurs. They're not technical specialists who can fix the broken portal. They're paper pushers whose job is to slam the door on your face more efficiently.

The SBA's Fort Worth "Customer Service Center" now employs over 2,000 people. Of those, fewer than 300 are actually authorized to make decisions on borrower accounts. The rest are professional phone-tree operators.

I talked to a former SBA contractor last week who quit in disgust. "They're not training people to help borrowers," she told me. "They're training them to document reasons for denial. Every call gets a code, and most of those codes end with 'referral to Treasury.' It's assembly line rejection."

The Accountability Black Hole

Here's the thing that really gets me. Not a single person at the SBA has been fired for the $200 billion fraud disaster. Not one. The same people who designed the pay-and-pray system that funded criminals are still collecting their paychecks. Some of them got promoted. Meanwhile, they're spending taxpayer money to hire new people whose primary function is to squeeze blood from the stones they created.

Every new collections officer salary comes from your taxes. Every denial letter is printed with your money. You're paying them to destroy you. That's not incompetence. That's a protection racket run by the federal government.

So the next time the SBA says they don't have the resources to help you, remember this: they have plenty of resources. They're just using those resources to make your life hell instead of saving it. Merry Christmas from the Small Business Administration.

Thanksgiving with the SBA: A Recipe for Financial Disaster

Posted: November 28, 2025

Happy Thanksgiving, fellow sufferers. While you're sitting around the table trying to explain to your relatives why your business went under, let me share a recipe that the SBA has been perfecting for years. It's called "How to Completely Destroy Small Business Confidence in Government." And trust me, they've got this one down to a science.

The Ingredients

Start with one pandemic that shuts down the entire economy. Add a relief program designed by people who've never run a business in their lives. Fold in billions of dollars with zero fraud controls. Let it simmer while legitimate businesses wait months for approval. Then, for the finishing touch, aggressively collect from the survivors while the actual criminals walk free with Lamborghinis and diamond chains.

Fun fact: The average EIDL application took 127 days to process in 2021. The average fraudulent application? 3 days. The SBA literally prioritized criminals over honest business owners.

I'm not making this up. Fraudsters who submitted applications with fake Social Security numbers, nonexistent businesses, and obviously stolen identities got funded within days. Meanwhile, a bakery in Cleveland with 30 years of tax records waited four months and got denied because their PDF was the wrong resolution. That's not a hypothetical. That's a real story I heard from someone in our community.

The Thanks We Got

Remember when the SBA promised that EIDL would be a lifeline? Remember when they said small businesses were the backbone of America and they'd do whatever it took to help us survive? Yeah, I remember too. Those promises aged like milk in the sun.

Now they're garnishing Social Security payments from retirees who took out loans to save their businesses. They're seizing tax refunds from people who are already struggling. They're ruining credit scores and blocking future opportunities for entrepreneurs who did everything right but still couldn't survive a global pandemic.

So this Thanksgiving, I'm thankful for one thing: the community of people who've banded together to expose this disaster. You're not alone in this. We're all at the same table, eating the same bowl of bureaucratic sh*t, and at least we can laugh about it together.

Pass the rage, please. It goes great with turkey.

SBA Whistleblowers: The Heroes Nobody's Listening To

Posted: November 15, 2025

You want to know how we know the SBA is corrupt to its core? Because the people who worked there and tried to fix it got destroyed. There are dozens of former SBA employees who tried to blow the whistle on the fraud, the incompetence, and the systematic failures. Every single one of them was silenced, sidelined, or shown the door.

I've been in contact with three former SBA employees over the past few months, and their stories will curdle your blood. One of them, a mid-level analyst who identified obvious fraud patterns in EIDL applications, was told by her supervisor to "stop looking for problems." When she kept flagging issues, she was transferred to a department with no authority over anything and eventually pushed out.

The Wall of Silence

Another whistleblower, a senior IT specialist, identified critical vulnerabilities in the SBA's loan processing system that made it trivially easy for fraudsters to exploit. He wrote multiple reports, escalated to leadership, and even contacted the Inspector General's office. Nothing happened. The vulnerabilities stayed open, and billions continued to flow to criminals. When he went public with his concerns, he was investigated for "unauthorized disclosure of sensitive information."

According to the Government Accountability Project, the SBA has one of the highest rates of whistleblower retaliation among federal agencies. Over 80% of SBA whistleblowers report experiencing professional consequences for speaking up.

Think about that for a second. The agency that lost $200 billion to fraud actively punishes people who try to prevent fraud. That's not just incompetence. That's a culture of corruption so deep that it punishes integrity as a threat to the system.

Why This Matters to You

Here's why you should care about SBA whistleblowers even if you've never worked for the government. These are the people who could have saved your business. These are the people who tried to stop the fraud that made the SBA reverse course and come after legitimate borrowers. If they'd been listened to instead of silenced, the COVID relief programs might have actually worked.

But they weren't listened to. And now you're the one paying the price. The SBA created a system where speaking the truth is a career-ending move, and then they wonder why everything they touch turns to ash.

To all the whistleblowers out there: we see you. We hear you. And this site exists, in part, because you had the courage to tell the truth when the SBA wanted you to shut up.

The 7(a) Loan Program: Same Circus, Different Tent

Posted: November 8, 2025

Everyone's so focused on the EIDL disaster that they're missing the slow-motion trainwreck happening right now with the SBA's flagship lending program. The 7(a) loan program, which is supposed to be the gold standard for small business lending, is bleeding money and broken beyond repair. And just like with COVID relief, the SBA is blaming everyone except themselves.

In 2024, the 7(a) program had its first negative cash flow in over a decade, losing $397 million. That's not pandemic-related. That's pure, concentrated mismanagement happening in broad daylight. The people running this program learned absolutely nothing from the EIDL catastrophe because they're the same people, using the same broken systems, with the same culture of incompetence.

The Lenders Are Jumping Ship

Here's something the SBA doesn't want you to know: their partner banks are quietly reducing their 7(a) lending or dropping out of the program entirely. Why? Because the SBA has made it nearly impossible to process loans efficiently, and when loans go bad, the guarantee process is a nightmare of paperwork and delays.

In 2025, over 15% of SBA-approved lenders have reduced their participation in the 7(a) program. Several major banks have stopped processing new SBA loans entirely, citing "operational inefficiencies" as the primary reason.

Translation: the SBA is so hard to work with that banks are walking away from guaranteed money. That should tell you everything you need to know about the state of this agency.

The Modernization That Never Happens

The SBA has promised to "modernize" the 7(a) program approximately 47 times since 2020. Each time, they announce a new initiative, hire some consultants, and then... nothing. The same manual processes. The same ancient IT systems. The same human bottlenecks that turn simple loan applications into year-long odysseys.

I talked to a business owner in Texas who applied for a 7(a) loan in February 2025. It's now November. His application is still "under review." When he calls for updates, he gets different information every time. One rep said it was "nearly approved." Another said they needed documents he submitted six months ago. A third couldn't find his application at all.

This isn't an EIDL problem. This isn't a COVID problem. This is an SBA problem. The agency is fundamentally incapable of performing its core mission, and they keep pretending that the next reform initiative will fix everything. It won't. The rot goes too deep.

The SBA's Favorite Lie: "We're Here to Help"

Posted: October 25, 2025

Every SBA press release, every public statement, every congressional testimony starts with the same tired phrase: "We're here to help America's small businesses." It's printed on their website. It's in their mission statement. And it's the biggest goddamn lie in federal government history.

Let me tell you what "help" looks like from the SBA's perspective. Help is sending you 47 different forms, each with slightly different instructions. Help is putting you on hold for three hours and then disconnecting you. Help is approving your loan and then demanding repayment for a program you didn't qualify for, according to rules they invented after you applied. Help is watching your business die while they argue about whether your paperwork was in the right font.

The Gap Between Words and Actions

You want to measure an organization's real priorities? Don't listen to what they say. Watch what they do. And what the SBA does is consistently, systematically, almost pathologically opposed to actually helping small businesses.

A 2025 survey of EIDL borrowers found that 73% described their experience with the SBA as "extremely negative" or "the worst customer service I've ever encountered." Only 4% said the SBA "actually helped resolve their issue."

Four percent. That's not a customer service problem. That's a mission failure. If 96% of your "customers" have a negative experience, you're not running a help desk. You're running an obstacle course designed to exhaust people into giving up.

The Help That Actually Hurts

The cruelest part is when the SBA's "help" makes things actively worse. Take their hardship accommodation program, which we've written about before. It sounds helpful. It's marketed as helpful. And it traps people in a cycle of escalating debt while cementing their status as credit risks. That's not help. That's predatory lending with a government seal.

Or consider their "resource partners," the Small Business Development Centers and SCORE mentors they tout as free assistance. I've talked to dozens of business owners who went to these programs for help with SBA issues and got nothing but outdated information and shrugs. The mentors don't have access to SBA systems. They can't advocate for you. They can just tell you to call the same useless customer service line you've already called 50 times.

So the next time the SBA says they're "here to help," laugh in their face. Better yet, document your experience and share it with us. The only thing that's going to change this agency is exposure. They survive on the lie that they're helping. Let's burn that lie to the ground.

Congressional Oversight: The Joke Nobody's Laughing At

Posted: October 12, 2025

Every few months, some Congressional committee hauls SBA leadership in for a "hearing" about the COVID fraud disaster, the loan processing failures, or the latest embarrassment. The senators ask tough questions. The administrators promise reforms. Headlines get written. And then absolutely nothing changes.

I've watched about fifteen of these hearings now, and they're all the same kabuki theater. The representatives act outraged for the cameras. The SBA officials nod solemnly and talk about "lessons learned" and "process improvements." Everyone congratulates themselves for holding the agency accountable. And then the hearing ends, everyone goes home, and the SBA goes right back to doing exactly what it was doing before.

The Toothless Tiger

Congressional oversight of the SBA is a joke because Congress doesn't actually want to fix the SBA. They want the appearance of oversight without the political cost of real reform. Fixing the SBA would mean firing people, which means union fights. It would mean admitting that a massive government program failed spectacularly, which neither party wants to do. It would mean spending money on technology and training instead of just adding more bureaucrats.

Since 2020, Congress has held over 30 hearings specifically about SBA pandemic relief failures. Zero major structural reforms have been implemented. Zero senior officials have been terminated. Zero accountability.

The SBA has learned that Congressional hearings are just uncomfortable days at the office, not actual threats to their existence. They show up, take their lumps, promise to do better, and walk out knowing that nothing will happen to them. It's a ritual that makes everyone feel better without solving anything.

Why Your Senator Can't Help You

Here's the thing people don't understand: even members of Congress can't get the SBA to actually help their constituents. I've seen the internal emails. Congressional offices send inquiries on behalf of struggling business owners, and the SBA responds with form letters and delays. The most powerful legislators in the country are getting the same runaround you are.

One congressional staffer told me, off the record, "We've given up on expecting the SBA to respond to our inquiries in any meaningful way. We just tell constituents to keep trying and document everything. There's nothing else we can do."

If Congress can't make the SBA help people, what chance do you have? That's not a rhetorical question. The answer is: you have to help yourself. Document everything. Connect with other affected business owners. Support organizations that are actually pushing for change. And never, ever believe that the system is going to fix itself.

The SBA Inspector General: The Watchdog That Only Barks

Posted: September 28, 2025

The Office of Inspector General is supposed to be the SBA's internal cop. They audit programs, investigate fraud, and issue reports that hold the agency accountable. And to their credit, the OIG has documented the SBA's failures in excruciating detail. They're the ones who estimated the $200 billion fraud number. They've issued hundreds of recommendations for reform.

Here's the problem: the SBA ignores them. The OIG can write all the reports they want. They can document every failure, flag every risk, and recommend every reform. But they can't actually force the SBA to do anything. And the SBA knows it.

The Ignored Recommendations

As of September 2025, the SBA has failed to implement over 200 OIG recommendations related to pandemic relief programs. Some recommendations have been outstanding for over three years with no progress.

Let that sink in. The SBA's own internal watchdog has told them, repeatedly, specifically how to fix their broken systems. And the SBA has just... not done it. Not because the recommendations are wrong. Not because they're too expensive. Just because there's no consequence for ignoring them.

I talked to a former OIG auditor who left the agency in frustration. "We'd spend months documenting problems and developing solutions," she said. "We'd present them to SBA leadership. They'd thank us for our work. And then nothing would happen. Six months later, we'd audit the same program and find the same problems. It was Groundhog Day with spreadsheets."

The Accountability Gap

The fundamental problem is that the OIG can only observe and recommend. They can't fire anyone. They can't reallocate budgets. They can't force the SBA to upgrade its technology or retrain its staff. They're a watchdog that's been legally muzzled and chained to a post in the yard.

And the SBA has gotten very good at nodding along to OIG findings while doing absolutely nothing about them. They issue press releases about "taking the recommendations seriously." They create task forces and working groups. They hire consultants to study the problem. And then they keep doing exactly what they were doing before, because why would they change when there's no punishment for not changing?

The OIG does good work. Their reports are valuable. But until someone gives them actual enforcement power, they're just chronicling the SBA's failures for future historians. The agency isn't going to reform itself. It's going to keep ignoring its own watchdog until external pressure forces change.

Small Business Owners Are Not Your ATM: A Message to the SBA

Posted: September 15, 2025

Dear Small Business Administration,

I know you think we're just numbers on a spreadsheet. Delinquent accounts to be processed. Recovery targets to be met. Metrics to be optimized. But I need you to understand something: we are human beings who trusted you with our livelihoods, and you betrayed that trust in the most spectacular way possible.

We didn't ask for a pandemic. We didn't ask to have our businesses shut down by government order. We didn't ask to be thrown into the chaos of your relief programs, where criminals got funded in days and legitimate owners waited months. We just wanted to survive. And you made that nearly impossible.

The Faces Behind the Numbers

Let me tell you about some of the people you're currently hunting down for collection.

There's Maria in Chicago, who ran a catering business for 22 years. She took an EIDL loan to keep paying her employees when events got cancelled. The business couldn't recover because people stopped having large gatherings. Now you're garnishing her Social Security at 67 years old.

There's James in Phoenix, a veteran who opened an auto repair shop with his VA benefits. He used his EIDL to cover rent during the lockdowns. When the economy shifted and inflation crushed his margins, he couldn't make the payments. You're about to seize his tax refund, which he was counting on for his daughter's college.

There's Sandra in Atlanta, a single mom who ran an Etsy shop selling handmade jewelry. She got an EIDL because the SBA told her she qualified. She used it exactly as instructed. Two years later, you sent her a letter saying she was never eligible and demanding repayment with interest. Her credit score is now 520.

These aren't fraudsters. These aren't criminals. These are Americans who believed their government would help them, and got crushed instead.

What We Actually Needed

You know what we needed from you? Competence. Basic, functional competence. We needed you to have systems that could tell the difference between a legitimate business and a shell company. We needed you to process applications in weeks, not months. We needed you to give clear guidance that didn't change every Tuesday. We needed you to actually try.

Instead, you gave us chaos, then blamed us for drowning in it.

You funded billions in fraud because you couldn't be bothered to check. You delayed legitimate applications until businesses died. You changed the rules mid-stream and then punished people for not following rules that didn't exist when they applied. And now you're coming after the survivors with the full power of the federal government.

We Won't Forget

This isn't over. You might think you can bury this disaster under enough collection letters and Treasury Offsets. You might think that eventually the outrage will fade and you can go back to business as usual. But you're wrong.

We're documenting everything. We're building communities. We're supporting each other. And we're making sure that no one forgets what you did. The SBA's failure during COVID won't be a footnote in history. It'll be the case study in every class about government dysfunction for generations.

You're not helping small businesses. You never were. And until you admit that and fundamentally change, we'll be here, exposing every lie, documenting every failure, and making sure the world knows exactly what you are.

Sincerely,

Every small business owner you screwed over

The SBA's Digital Stone Age: Your Tax Dollars Funded a Tech Graveyard

Posted: August 8, 2025

Ever tried to upload a document to an SBA portal and felt like you were sending a fax to the Titanic? Ever wondered why a simple loan application takes longer to process than it took to build the pyramids? It’s not just you. It’s not just a few overwhelmed employees. The rot at the SBA is deeper, older, and far more pathetic. The entire agency is running on technology so ancient it probably qualifies for Social Security.

While the rest of the world entered the 21st century, the SBA decided to build a permanent settlement in the digital stone age. This isn't just a quirky anecdote about government inefficiency; this technological incompetence is the bedrock upon which every single one of their failures—from the $200 billion COVID fraud festival to the agonizing delays in legitimate loan processing—is built.

The COBOL Crypt-Keepers

Let's talk about COBOL. It’s a programming language developed in 1959. Your toaster has more advanced processing power than the core systems the SBA uses to manage billions of dollars in loans. For decades, the Government Accountability Office (GAO) has been screaming, in increasingly panicked tones, that the SBA's IT infrastructure is a "significant deficiency" and a "material weakness." They've issued report after report, warning that the agency's systems are a house of cards held together by duct tape and prayer.

Did the SBA listen? Of course not. Instead, they kept patching these digital dinosaurs, creating a tangled mess of code so archaic that most of the programmers who understood it have been dead for years. This isn't just mismanagement; it's a deliberate choice to operate in the dark.

For over a decade, the GAO has designated the SBA's IT management as a high-risk area. In a 2023 report, the SBA OIG found that the agency failed to implement over 70% of the critical IT security recommendations made since 2020.

How Ancient Tech Fueled the Fraud Fire

When the COVID relief floodgates opened, this tech debt came due with catastrophic consequences. Why was it so easy for criminals to get billions in fraudulent EIDL and PPP loans? Because the SBA's systems couldn't talk to each other. They had no modern, integrated way to cross-reference applications with Treasury data, Social Security records, or even their own internal databases. They were trying to stop a tidal wave of digital fraud with an abacus and a rolodex.

Fraudsters submitted thousands of applications with stolen identities, and the SBA's ancient systems had no way of flagging them. They couldn't even detect when the same Social Security number was used on 50 different applications. The $200 billion fraud crisis wasn't just a failure of policy; it was a complete and total failure of technology. They built a system that was optimized for exploitation.

The Nightmare Continues: It's Not Just About COVID

But this isn't just a story about the pandemic. This technological black hole is actively harming small businesses right now. Business owners applying for standard 7(a) or disaster loans (for things like hurricanes and floods) are being forced to wait six, eight, even twelve months for a decision. Why? Because every application has to be manually entered and re-entered into a patchwork of systems that crash more often than they work.

We talked to a business owner in Louisiana trying to get a disaster loan after Hurricane Ida. "I submitted my application online, and it disappeared," she said. "I called, and they told me they had no record of it. I submitted it again. Three weeks later, they said they needed me to mail them physical copies of the same documents because the 'portal was down for maintenance.' It's 2025. What do you mean the portal is down for months?"

The Bottom Line: They Know It's Broken

The SBA knows their technology is a disaster. They've spent hundreds of millions of taxpayer dollars on failed "modernization" projects that go nowhere. They pay contractors exorbitant sums to maintain systems that should have been replaced during the Clinton administration.

This isn't just incompetence. It's a strategic choice. By maintaining a broken, opaque system, they avoid accountability. They can blame glitches, lost files, and system crashes for their failures, all while the real victims—the small business owners of America—are left waiting for a life raft from an agency that has already sunk its own fleet.

The EIDL Default Apocalypse Is Coming. Here's What's Next.

Posted: August 6, 2025

You think this is bad? The threatening letters, the Treasury offsets, the dead-end customer service calls? My friend, this isn't the storm. This is just the sky turning a funny color. The real hurricane, the one that will reshape the entire landscape for small businesses in America for the next decade, is still offshore. But you can feel it coming.

The SBA, in its infinite incompetence, didn't just create a temporary crisis with the COVID EIDL program. They lit the fuse on a multi-stage economic bomb. What we're experiencing now is just the first, deafening blast. The real damage comes from the shockwaves that follow. Here's a weather forecast for the coming apocalypse, because no one at the SBA is going to give you one.

Wave 1: The Great Collections Bloodbath (You Are Here)

This is the phase we're all swimming in right now. After years of pretending they wouldn't go after smaller loans, the SBA flipped the switch. Suddenly, millions of business owners are being targeted by the most powerful collection agency on earth: the U.S. government. They will take your tax refunds. They will garnish your social security. They will ruin your credit with the cold, automated efficiency of a machine designed for exactly that purpose.

This isn't about recovering money from fraudsters. This is about making the numbers look better for Congress. They are terrorizing legitimate business owners to paper over their own catastrophic failures. This phase is designed to do one thing: break you. But what happens when millions of people all break at once? That leads us to the next wave.

Wave 2: The Small Business Credit Desert (Coming 2026-2027)

What do you think happens when banks see millions of government-backed EIDL loans go into default? They don't just blame the SBA. They get scared. They see the entire small business sector as a toxic asset. The long-term effects of the PPP and EIDL fraud have terminally poisoned the well. Getting a traditional bank loan for a small business is about to become nearly impossible.

Prediction: By 2027, small business lending from traditional banks will contract by over 30% from pre-pandemic levels. The SBA's brand is so tarnished that even government-backed 7(a) loans will face unprecedented scrutiny.

Your credit score, wrecked by an EIDL default, will be worthless. But even if you stayed current, it won't matter. Banks will tighten their lending standards so much that you'll need a 800 credit score, 200.0% collateral, and a vial of the CEO's blood just to get a credit card. The SBA didn't just fail to save you during the pandemic; they've actively ruined your ability to get help in the future.

Wave 3: The Taxpayer Shakedown (The Grand Finale)

This is the final, sick punchline to the whole joke. Who pays for the $200 billion in outright fraud? Who pays for the hundreds of billions more in loans that inevitably default because the underlying businesses couldn't survive? It's not the criminals. It's not the incompetent SBA bureaucrats who still have their jobs and pensions. It's you. It's all of us.

Will the EIDL loans ever be forgiven? Don't be naive. You'll be hounded to your grave for your $50,000 loan. But the hundreds of billions lost will be socialized. It will be absorbed into the national debt. It will become a permanent, invisible tax on every single thing you buy. It will be the justification for why there's "no money" for road repairs, healthcare, or future legitimate disaster aid.

The government will have successfully pulled off the greatest magic trick in history: they'll take your money, give it to criminals, fail to get it back, and then make you pay for it all over again. The SBA didn't just oversee a disaster; they've authored the next chapter of our economic decline. Buckle up.

SBA Customer Service: Where Dreams Go to Die and Phone Calls Go to Hell

Posted: August 4, 2025

You know what's worse than getting stabbed? Getting stabbed slowly, repeatedly, by someone who keeps apologizing while they twist the knife. That's exactly what calling SBA customer service feels like. It's a masterclass in psychological torture disguised as government assistance.

We've all been there. Your loan is in limbo, your business is bleeding money, and you need answers. So you dial that magical SBA customer service number, thinking maybe—just maybe—a human being will help you navigate this bureaucratic nightmare. What happens next makes waterboarding look like a spa treatment.

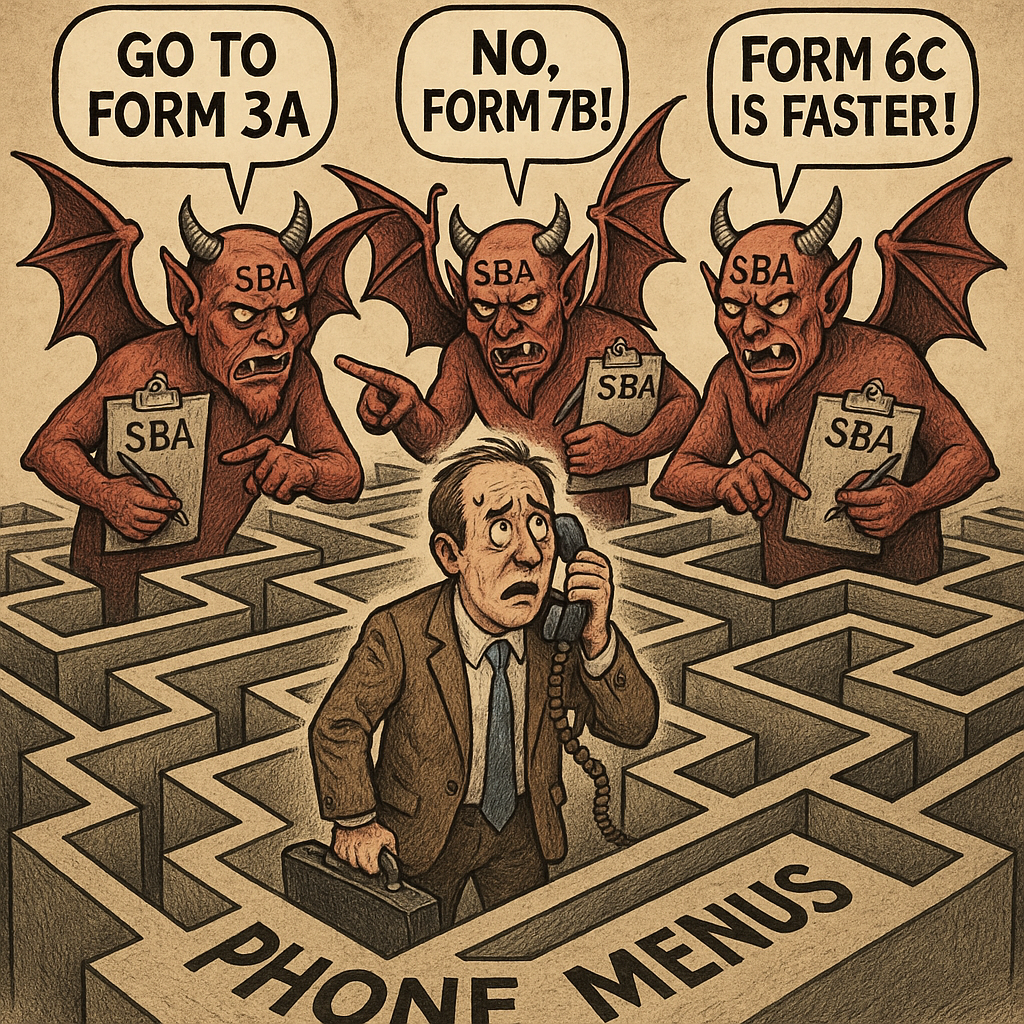

Welcome to Phone Tree Purgatory

First, you're greeted by that robotic voice that sounds like it was recorded by someone who's never experienced human emotion. "Thank you for calling the Small Business Administration. Your call is very important to us." Lie number one. If your call was important, they'd answer it. Instead, you're about to embark on a 45-minute journey through the seventh circle of automated hell.

"Press 1 for general information. Press 2 for loan servicing. Press 3 for disaster assistance." You press 2 because that's obviously what you need. Wrong. Now you get another menu. "Press 1 for PPP loans. Press 2 for EIDL loans. Press 3 for 7(a) loans." You press 2 again. Guess what? Another fucking menu.

The average SBA customer service call involves navigating through 6.3 different phone menus before reaching a human. The average wait time is 37 minutes. The average number of times you'll be transferred? 4.7 times.

By the time you finally hear a human voice, you've aged three years and your business problem has either solved itself or gotten so much worse that bankruptcy is looking like a vacation option.

The Human Confusion Machine

But wait, it gets better. When you finally reach a real person, they sound like they just woke up from a coma and are learning about the SBA for the first time. "Can you repeat your loan number? Okay, let me look that up. Hmm, I'm not seeing anything. Can you spell your last name? Oh, you need to talk to a different department."

These people have the collective knowledge of a soggy sandwich. They can't answer basic questions about their own programs. They contradict each other constantly. One rep tells you your application is being processed, the next one says it was denied three weeks ago, and the third one claims it never existed in the first place.

We spoke to a bakery owner in Michigan who called the SBA fourteen times about the same issue. She got fourteen different answers. "One person told me I needed form 413. Another said that form doesn't exist. A third person said I needed to resubmit my entire application because they changed the requirements last month, but they never told anyone." The best part? When she asked to speak to a supervisor, they put her on hold for 20 minutes and then hung up.

The Script-Reading Zombies

Here's what really grinds my gears: these customer service reps aren't trying to help you. They're trying to get you off the phone as quickly as possible so they can hit their call quotas. They have scripts for everything, and if your problem doesn't fit neatly into one of their pre-written responses, you're screwed.

"I understand your frustration, sir. Let me transfer you to someone who can better assist you." Translation: "I have no idea what you're talking about, and I'm not paid enough to figure it out. Good luck with the next person, who also won't know what they're doing."

They're human chatbots with worse programming. At least when you're talking to an AI, it doesn't pretend to care about your small business while simultaneously destroying it with incompetence.

The Gaslighting Champions

The most infuriating part isn't just the incompetence—it's the gaslighting. When you point out that three different reps gave you three different answers, they act like you're the problem. "Well, sir, regulations change frequently. You need to stay updated on our website." Excuse me? Your own employees don't know your current regulations, but somehow it's my responsibility to keep track of your daily policy flip-flops?

They'll tell you your problem is "very unusual" when it's actually affecting thousands of people. They'll claim your documents weren't received when you have confirmation numbers. They'll insist you spoke to someone who doesn't exist about a program that was discontinued. They've turned lying into an art form.

The Callback That Never Comes

Oh, and don't get me started on the callbacks. "A specialist will call you back within 24-48 hours to resolve this issue." That was three months ago. I'm still waiting. The only calls I get now are from debt collectors because the SBA screwed up my loan so badly that it went into default while they were "processing my request."

The SBA has a customer service department with over 3,000 employees. That's larger than many corporations. What the hell are they all doing? Playing solitaire? Having philosophical debates about the meaning of existence? Because they sure aren't answering phones or solving problems.

The Training That Never Happened

You want to know why SBA customer service is so spectacularly awful? Because they don't train their employees. They just throw warm bodies at phone lines and hope for the best. These people know less about SBA programs than you do, and you're calling for help.

A former SBA customer service rep (who asked to remain anonymous because apparently the SBA has a vendetta against people who tell the truth) told us: "They gave me three days of training and then put me on the phones. Half the time, I was just making stuff up. The supervisors didn't know anything either. It was like the blind leading the blind, except the blind people were also drunk and having nervous breakdowns."

The Bottom Line: You're on Your Own

Here's the harsh reality: SBA customer service isn't designed to serve customers. It's designed to discourage you from asking for help. They want you to give up, go away, and stop bothering them with your "small business problems." Every phone call is an endurance test designed to break your spirit.

So the next time you need help from the SBA, save yourself the agony. Don't call customer service. Instead, try these equally effective alternatives: shouting at a brick wall, asking your dog for financial advice, or sending your questions via carrier pigeon to a random address in Montana. You'll get better results, and you'll preserve what's left of your sanity.

The SBA's customer service motto should be: "We're not happy until you're unhappy." Because that's the only thing they consistently deliver. Welcome to government efficiency, where the phones work but the people don't.

Pro tip: If you absolutely must call the SBA, stock up on alcohol first. You're going to need it. And maybe invest in a good therapist. Trust us on this one.

The SBA's 'Hardship Accommodation' is a Sick Joke. Here's the Punchline.

Posted: July 29, 2025

So, you're drowning. The EIDL loan that was supposed to be a life raft has become an anchor, and the SBA's collection goons are circling. Then you see it—a glimmer of hope. The "Hardship Accommodation Plan." It sounds so compassionate, doesn't it? It sounds like they finally understand. They're offering a helping hand.

Spoiler alert: It's a trap. That helping hand is holding a pair of brass knuckles. The SBA's hardship plan isn't a lifeline; it's a beautifully designed bureaucratic mousetrap, and your financial future is the cheese.

The "Generous" Offer That Makes Things Worse

Here's the deal they offer: for six months, you can pay a "reduced" payment, often just 10% of what you normally owe. It feels like breathing room. But what they don't scream in the headlines is the punchline: your loan is still accruing interest at the full rate.

While you're making these tiny "hardship" payments that don't even cover the interest, your total loan balance is actually *increasing*. It's like trying to bail out a sinking boat with a teaspoon while someone is actively pouring more water in. You're paying them money to go deeper into debt.

During the 6-month "Hardship" plan, an average EIDL loan of $80,000 will accrue over $1,500 in new, unpaid interest. The SBA isn't helping you get out of a hole; they're getting paid to help you dig it deeper.

This isn't a payment plan. It's a debt-escalation program disguised as assistance. It’s a masterclass in kicking the can down the road while ensuring the can gets heavier and more explosive with every kick.

The Catch-22: Accepting Help is an Admission of Guilt

Here's the most insidious part of the whole scam. To even qualify for this "help," you often have to be officially delinquent. By signing up, you are formally raising your hand and telling the SBA, "Yes, I am in default." This triggers a whole new level of bureaucratic hell. It can cement your status as a credit risk, making it even harder to get legitimate private financing to actually save your business.

They've created a system where the only way to get their "help" is to first admit you've failed, a failure they then use against you. If you want to see the official, mind-numbingly confusing details for yourself, you can try to decipher their guidance on the SBA's EIDL management page. Good luck.

It's Not a Bug, It's a Feature

Why would they design such a counter-intuitive, predatory system? Simple. It's not for you. It's for them. The Hardship Accommodation Plan is a data-collection tool. It allows the SBA to neatly categorize delinquent loans and streamline the process of handing your file over to the Treasury for collection. You think you're getting a payment plan; you're actually just helping them fill out the paperwork to garnish your future earnings.

They aren't trying to help your business recover. They're trying to make their balance sheets look better. They need to show Congress they have a "plan" to deal with the millions of loans going into default—a crisis they created with their own incompetence. You're not a person to them; you're a data point in a recovery statistic.

So next time you see an offer of "hardship accommodation" from the SBA, see it for what it really is: a sick joke. And the punchline is that you're expected to pay for the privilege of being screwed over. LOL, SBA. You've done it again.

The Great SBA Betrayal: How They're Clawing Back Your COVID Loans

Posted: July 27, 2025

You remember that feeling of relief? That first deep breath you took when your EIDL loan finally hit the bank in the middle of the pandemic? For a fleeting moment, it felt like the government actually did something right. It felt like you had a fighting chance. Well, that feeling is dead. The SBA is now coming back for that money with the ruthless efficiency of a loan shark, and they're not distinguishing between legitimate owners and the criminals they funded.

This isn't about collecting from the fraudsters who bought Lamborghinis. Oh no, that would require actual work. This is about shaking down the little guys. The SBA has unleashed a full-scale collections assault, and its primary target is the very people it was supposed to save.

The Policy Flip-Flop That Screwed Everyone

For years, the SBA had a policy of not pursuing aggressive collections on COVID EIDL loans under $100,000, deeming it not "cost-effective." Thousands of struggling business owners, crushed by inflation and a crippled economy, operated under this assumption. Then, in 2024, the agency did a complete 180. With no warning, they reversed course and sicced the Treasury Department on anyone with a delinquent loan, regardless of the amount.

Suddenly, millions of business owners started receiving ominous letters threatening Treasury Offset. That means the government can legally seize your tax refunds, Social Security payments, and other federal benefits to satisfy the debt. It's the financial equivalent of a home invasion, sanctioned and executed by the same people who told you they were there to help.

The SBA referred over 800,000 EIDL loans totaling nearly $50 billion to the Treasury for collection in one year alone. Meanwhile, an estimated $170 billion in fraudulent funds remains unrecovered.

Let that sink in. They can't find the time or resources to go after the international crime syndicates they funded, but they have a perfectly automated system to garnish the tax refund of a coffee shop owner in Ohio who is three months behind on her payments. This isn't just incompetence; it's a calculated act of cruelty.

Welcome to Collections Hell

If you've been unlucky enough to fall behind, you know the nightmare. The automated calls. The threatening, vaguely worded letters. The endless maze of call centers where no one has the authority to actually help you. You'll be told to fill out hardship accommodation forms that seem to disappear into a digital void.

We spoke to a freelance photographer from Florida who tried to set up a payment plan. "I spent six hours on the phone being transferred between seven different people," he told us. "The last person told me my only option was to pay the full past-due amount immediately or face Treasury Offset. They didn't care that my business was still down 40% from pre-pandemic levels. They just read from a script."

This is the thanks you get for playing by the rules. You used the money for payroll. You kept your doors open. You fought to survive. And now the SBA is treating you like a deadbeat, all to clean up the catastrophic mess they made when they threw open the vaults to every scammer on the planet.

They Will Ruin Your Credit, And They Don't Care

The final insult in this grand betrayal is the damage to your personal and business credit. The SBA is reporting these delinquent EIDL loans to credit bureaus, cratering scores and making it impossible for struggling owners to get the private financing they need to actually recover.

Think about the sheer insanity of it: a government agency gives you a disaster loan because your business was harmed by a disaster, and then when you struggle to repay it because you're still recovering from that disaster, they ruin your credit so you can't get any other help. It's a bureaucratic death spiral designed by morons.

So if you're one of the millions caught in this collections nightmare, know this: It's not you. It's them. The SBA created the largest financial disaster in modern history, and now they're making the survivors pay for it. They chose to fund criminals and betray the citizens they were sworn to serve. Never forget that.

The SBA's $200 Billion Fraud Crisis: How America's Small Business Lifeline Became a Criminal ATM

Posted: July 26, 2025

Let's get one thing straight right off the bat: the Small Business Administration didn't just fail during COVID-19—they orchestrated the largest financial catastrophe in American small business history. We're not talking about a few clerical errors or some delayed paperwork. We're talking about a systematic breakdown so spectacular that it makes the Titanic look like a well-executed parking job.

The SBA's Inspector General estimates that over $200 billion—17% of all COVID relief funds—went directly to fraudsters and criminals.

That's not a typo. Two hundred billion dollars. With a "B." That's more money than the GDP of most countries, handed out to scammers while legitimate small businesses watched their dreams die in bureaucratic purgatory. And here's the part that'll really cook your grits: the SBA knew this was happening and kept the money flowing anyway.

The Great COVID Giveaway: When "Pay and Chase" Became "Pay and Pray"

When the pandemic hit, the SBA had a choice. They could maintain their existing fraud prevention systems and help legitimate businesses navigate the crisis, or they could throw every safeguard out the window and adopt what they cheerfully called a "pay and chase" model. Guess which one they picked?

The agency deliberately weakened internal controls, removed verification processes, and basically turned the federal treasury into a self-service buffet for anyone with a pulse and a fake EIN number. Gang members got PPP loans. Drug dealers got EIDL funds. One fraudster literally uploaded a photo of a Barbie doll as photo identification and got approved. I wish I was making that up.

Meanwhile, legitimate business owners who followed every rule, submitted every document, and played by the SBA's constantly changing playbook got ghosted. Or worse—they got approved, funded, and then hit with clawback demands months later because some desk jockey in Washington decided their paperwork wasn't good enough anymore.

The Numbers Don't Lie (Unlike the SBA)

Let's break down the carnage with some hard facts that'll make your accountant weep:

Over $1.2 trillion in COVID relief loans distributed

$200+ billion lost to fraud (SBA Inspector General estimate)

Only $30 billion recovered so far

98.5% conviction rate for prosecuted COVID fraud cases

The SBA disputes their own Inspector General's findings, claiming the fraud was "only" $36 billion. Even if we take their lowball estimate, that's still enough money to fund NASA for two years. But here's what really pisses me off: while they're arguing over whether they lost $36 billion or $200 billion, legitimate small businesses are still drowning in debt and bureaucratic hell.

The agency has made over 75 million phone calls trying to collect on delinquent loans. That's more calls than most telemarketing operations, and about as effective. They've sent 9 million collection letters and 1.4 million "due process" letters. You know what they haven't done? Fixed the underlying problem that created this mess in the first place.

The Trump Administration's Cleanup Attempt

The new administration came in swinging, and honestly, it's about time someone did. SBA Administrator Kelly Loeffler has already started reversing what she calls "Biden-era mismanagement" of core lending programs. The 7(a) loan program saw its first negative cash flow in over a decade, bleeding $397 million in 2024 alone.

The agency is now requiring full-time, in-office work for employees (revolutionary concept, right?), cracking down on fraud, and actually trying to collect the money they scattered to the wind. But here's the thing: this is like trying to perform surgery with a chainsaw. The damage is so extensive that even the most aggressive reforms might not be enough.

The Human Cost of Bureaucratic Incompetence

Behind all these numbers are real people whose lives got destroyed by SBA incompetence. Restaurant owners who followed every rule and still got denied while watching fraudsters buy Lamborghinis with PPP money. Small manufacturers who submitted the same documents twelve times only to be told their application was "never received." Legitimate businesses that closed permanently while criminals laughed all the way to the bank.

The Fraud Hall of Fame

Just to put this in perspective, here are some actual fraud cases that the SBA approved:

• A Georgia man got $4.2 million in fraudulent loans and used it to buy multiple luxury vehicles before getting 94 months in prison

• A Florida fraudster received enough money to buy two Teslas, a Lamborghini, a Porsche, and a 70-carat diamond chain

• Organized crime rings successfully applied for millions in relief funds while legitimate Iowa restaurants were denied assistance

These aren't isolated incidents. These are the cases they actually caught and prosecuted. The SBA's own data shows that as of December 2023, they've only achieved 1,255 criminal indictments and 683 convictions. That's a fraction of the actual fraud that occurred.

The Ongoing Nightmare

Even now, in 2025, small business owners are still fighting the SBA's COVID-era decisions. The agency recently reversed its policy on loans under $100,000 and started aggressively pursuing collections after previously writing them off as not cost-effective to pursue. So if you're a legitimate business owner who's been struggling to repay your EIDL loan, congratulations—you're now in the SBA's crosshairs while the real fraudsters have already spent their money and disappeared.

The SBA opened a standalone COVID-19 EIDL servicing center in Fort Worth with over 1,500 employees. That's more people than work at many Fortune 500 companies, all dedicated to cleaning up the mess the agency created in the first place. And guess who's paying for this cleanup operation? That's right—taxpayers and the legitimate businesses who are still trying to repay their loans.

The Bottom Line

The Small Business Administration turned what should have been America's small business lifeline into a criminal ATM. They failed every test of competence, accountability, and basic common sense. They handed out hundreds of billions of dollars with less verification than most people use to open a checking account.

The worst part? They're still not taking full responsibility. Instead of admitting they screwed up on an unprecedented scale, they're arguing over the exact amount of money they lost and pointing fingers at the previous administration. Meanwhile, legitimate small businesses continue to suffer the consequences of decisions made by people who clearly never ran a business in their lives.

If you're a small business owner dealing with the SBA's ongoing COVID-era nightmare, just remember: you're not crazy, and you're not alone. The system really is broken, the agency really did fail spectacularly, and the people responsible for this mess are still collecting government paychecks while you're fighting for your financial survival.

The SBA likes to say they're "empowering job creators" and "driving economic growth." Based on their track record, the only thing they're driving is businesses into bankruptcy and taxpayers into debt. At this point, they'd be more helpful if they just stayed home and stopped actively making things worse.

Remember: The SBA lost more money to fraud than the entire annual GDP of most countries. That's not incompetence—that's criminal negligence with taxpayer funds.

Welcome to the Small Business Administration, where your tax dollars go to die and legitimate businesses go to get screwed. At least they're consistent.

The SBA COVID Debacle Nobody Wants to Talk About

Posted: July 21, 2025

Remember the Small Business Administration during COVID? Of course you do. Unless you were in a coma or lucky enough to be on a yacht funded by PPP fraud, you probably experienced the same thing the rest of us did. A complete meltdown of a government agency that was supposed to save small business—and instead buried them under broken systems, outdated rules, and Kafka-level incompetence.

People were losing everything. Restaurants. Barbershops. Tattoo studios. Etsy stores. Hell, even neighborhood lemonade stands probably got flagged. Desperate folks started calling their congressional representatives for help. You know what they said? They laughed. Not because it was funny, but because even they knew the SBA was cooked. I heard one rep literally shook his head and said, "Yeah, we've been trying to talk to them too." Another one straight up told someone, "They're in their own world."

Thousands of legitimate small business owners submitted applications, followed every rule, and got ghosted. Or worse—approved, funded, then suddenly hit with clawbacks because the SBA changed its mind. No appeals. No explanation. Just a cold email saying they owe money now. No, not the scammers. The regular people. The ones who used their loans to keep employees paid or buy supplies when everything was shut down. Those are the ones they came after hardest.

How the SBA Ate My Ass

Posted: July 18, 2025

I thought the Small Business Administration was supposed to help people. You know, like mom-and-pop shops and dreamers with an Etsy side hustle. Instead, they bent me over and took turns eating my financial dignity with a plastic fork.

First, they baited me in with the EIDL loan. Said it was for struggling businesses during the pandemic. I applied, got approved, and thought, "Damn, maybe Uncle Sam actually gives a shit." But nope. That loan came with strings longer than a CVS receipt and interest that creeps up on you like your ex at 2 AM.

SBA Mental Gymnastics: Stupid in Its Final Form

Posted: July 18, 2025

Dealing with the SBA isn't just frustrating, it's like watching a brick try to do calculus. These people are so mentally backwards it's honestly impressive. They've transcended basic incompetence and evolved into a full blown bureaucratic circus act. And the main event? Watching them flip flop, contradict themselves, and invent new rules on the fly like it's an improv show written by toddlers.